Cerebras Systems Inc. has filed for an initial public offering on the Nasdaq under the ticker...

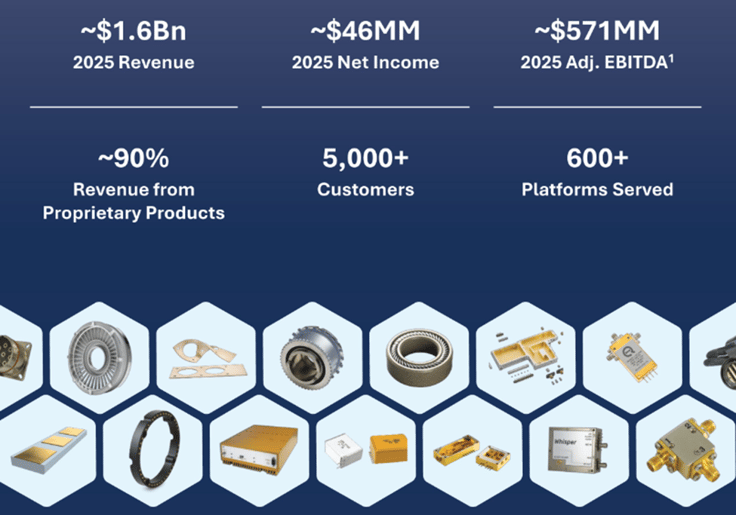

Arxis, Inc. has filed to go public on the Nasdaq under the ticker ARXS, offering 37.7 million shares at a price range of $25.00 to $28.00, implying a deal size of approximately $1.0 billion at the midpoint and a post-offer market capitalization of approximately $1.6 billion. The offering is being led by Goldman Sachs, Morgan Stanley and Jefferies, with shares expected to list on the Nasdaq Global Select Market.

Arxis is positioning itself as a scaled, differentiated supplier of mission-critical electronic and mechanical components used across aerospace, defense, medical technology and advanced industrial applications. The company has been built through a deliberate acquisition strategy led by Arcline, combining more than 30 businesses since 2019 into a unified platform centered on proprietary, engineered products designed for high-performance and high-reliability environments.

At the core of the story is a “designed-in” revenue model, where components are embedded into customer platforms early in the development cycle and remain in place for decades. Approximately 90% of revenue is derived from proprietary products, which typically represent a small portion of total system cost but are critical to performance, creating high switching costs and durable pricing power. Arxis serves more than 5,000 customers across over 600 platforms, resulting in a highly diversified and deeply embedded revenue base where no single customer or program dominates. This combination of proprietary content, broad customer reach and long-duration platform exposure supports recurring revenue, aftermarket participation and strong visibility over time.

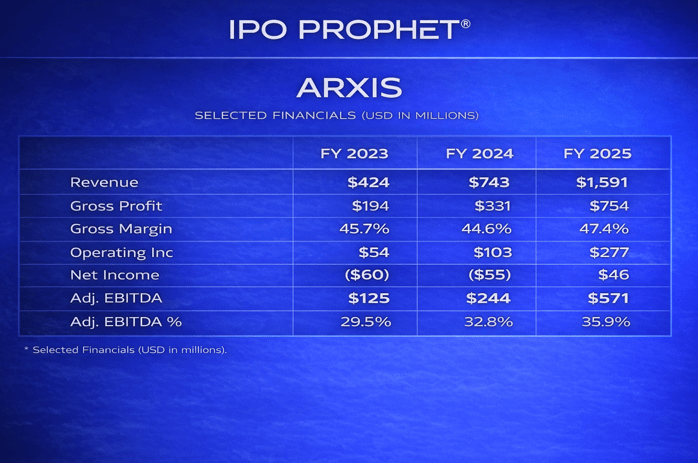

Financially, Arxis generated approximately $1.6 billion of revenue in 2025, alongside $46 million of net income and roughly $571 million of adjusted EBITDA, reflecting a high-margin profile supported by engineered differentiation and operational scale. The business has inflected from losses in prior years to profitability in 2025, with margin expansion driven by integration, pricing and operating leverage following its multi-year consolidation strategy.

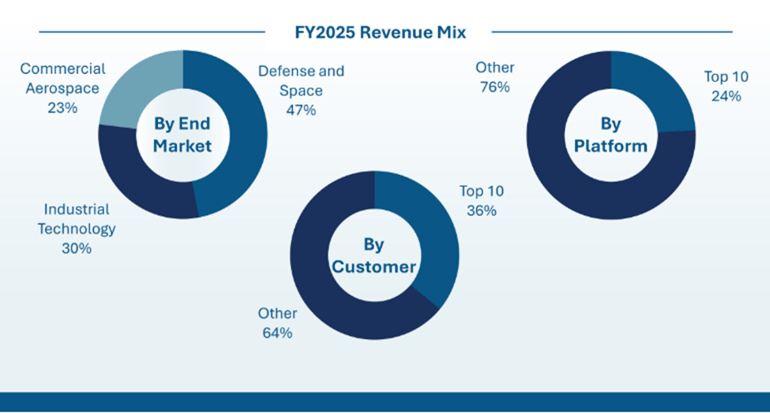

The company operates across two primary segments—Electronic Components (~44% of revenue) and Mechanical Components (~56%)—with end market exposure led by defense and space (~47%), followed by commercial aerospace (~23%) and diversified industrial and medical sectors. This mix positions Arxis to benefit from sustained defense spending, aerospace recovery and increasing system complexity across industrial and healthcare applications.

Strategically, Arxis emphasizes its “layer cake” model, where thousands of small, engineered component wins accumulate into a highly recurring and visible revenue base over long platform lifecycles. This is supported by its internally developed Arxis EDGE operating system, which drives cross-selling, pricing discipline and acquisition integration across its decentralized business units, forming the backbone of its growth strategy.

From a comps perspective, Arxis aligns most closely with high-performance aerospace and defense component suppliers such as TransDigm and HEICO, where valuation frameworks are often driven by IP content, aftermarket exposure and margin durability. While Arxis exhibits several of these characteristics, including high proprietary content and embedded revenue streams, investors will likely focus on its ability to sustain organic growth and continue executing on its acquisition-driven model post-IPO.

The offering is further supported by a group of high-quality cornerstone investors, including Capital International Investors, Capital Research Global Investors, Janus Henderson and T. Rowe Price, which have indicated interest in purchasing up to $400 million of shares, representing approximately 40% of the deal at the midpoint. While non-binding and not subject to lock-up agreements, the presence of these large, long-only institutions provides an important signal of early demand and may help anchor the order book, particularly given the scale of the offering. At the same time, the flexibility around participation and absence of lock-ups introduces some uncertainty around final allocations and post-IPO trading dynamics, making the quality of broader institutional demand a key factor to watch as the deal progresses.

Risk factors center around the company’s exposure to aerospace and defense cycles, dependence on continued acquisition execution and integration, and its post-IPO governance structure. Following the offering, Arcline-affiliated entities are expected to retain over 99% of voting control, limiting influence for public shareholders and reinforcing the company’s status as a controlled entity.

Overall, Arxis enters the public markets as a scaled, sponsor-built platform combining engineered product differentiation with a repeatable acquisition playbook, offering investors exposure to resilient end markets and high-margin components, while carrying the execution and governance considerations typical of private equity-backed IPOs.

Arxis is expected to officially go public on Thursday, April 16th.