Kardigan, Inc. (KARD) has filed for an initial public offering of 23.33 million shares at a price...

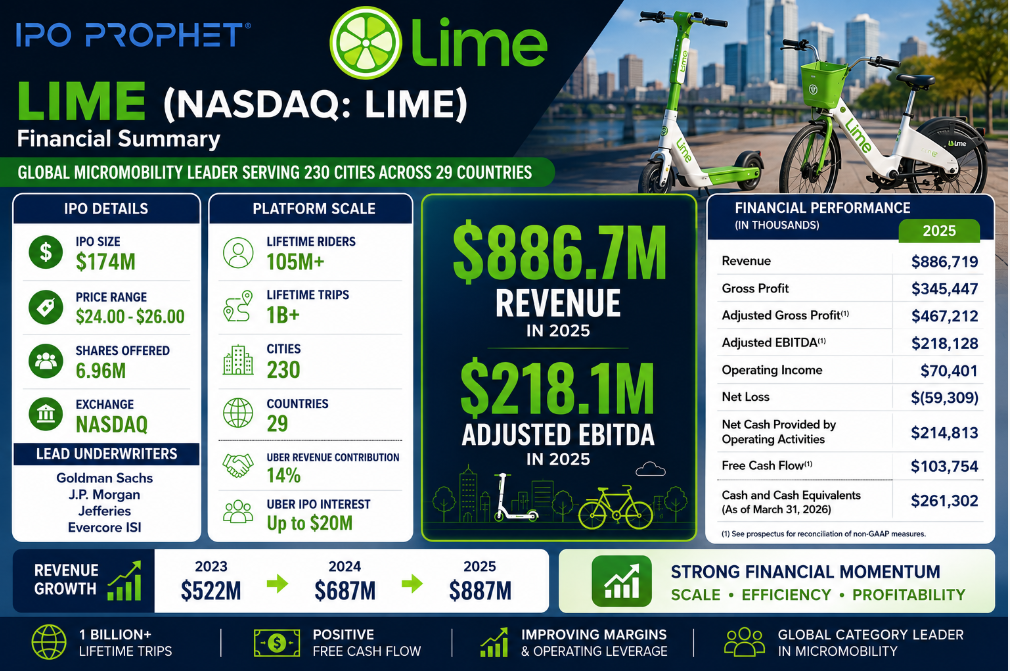

Lime, formally Neutron Holdings, Inc. (NASDAQ: LIME), has filed for an initial public offering of 6.96 million shares at a proposed price range of $24.00 to $26.00 per share. The company is selling 6.68 million shares, with selling stockholders offering an additional 276,731 shares. At the midpoint price of $25.00, the offering would raise approximately $174 million in gross proceeds. Lime has applied to list on the Nasdaq Global Select Market under the ticker LIME. The offering is being led by Goldman Sachs, J.P. Morgan, Jefferies, Evercore ISI, Citizens Capital Markets, KeyBanc Capital Markets, Needham & Company and William Blair.

Lime is the largest global shared micromobility platform, providing short-term rentals of electric scooters and electric bikes across approximately 230 cities in 29 countries. The company has served more than 105 million lifetime riders and completed more than one billion lifetime trips, establishing Lime as one of the most recognized brands in urban transportation. Its platform is designed around shared, affordable and lower-emission transportation, positioning the company at the intersection of urban mobility, sustainability and smart-city infrastructure.

The company's business model is built around a vertically integrated technology platform that combines proprietary hardware, software, fleet operations, data science, government relations and city-level operating expertise. Lime designs and manages its own vehicles, controls the rider experience through its app and operating systems, and uses data generated across its global network to improve fleet placement, reliability, utilization and safety. This integration gives the company more control over unit economics than earlier micromobility models that relied heavily on third-party hardware and less mature operating infrastructure.

Lime's investment thesis is centered on scale, density and operating leverage. As rider adoption increases in a city, fleet utilization improves, service reliability increases and vehicle density becomes more efficient. That creates stronger local economics, which supports additional fleet investment and improved availability. The result is a network effect at the city level, where more riders and more vehicles can reinforce one another while also helping cities expand alternatives to private car usage.

The company also benefits from a strategic relationship with Uber. Lime vehicles are integrated into the Uber app in most shared markets, giving Lime access to Uber's global user base and providing an additional customer acquisition channel. Revenue generated through Uber represented approximately 14% of total revenue in 2025, making the relationship meaningful but not overwhelmingly concentrated. Entities affiliated with Uber have also indicated interest in purchasing up to $20 million of shares in the IPO.

Financial performance has improved materially over the last three years. Revenue increased from $522.0 million in 2023 to $686.6 million in 2024 and $886.7 million in 2025, representing growth of 31.5% in 2024 and 29.1% in 2025. The 2025 increase was driven by an 18% increase in average operational fleet, a 21% increase in monthly active users and a 10% increase in revenue per vehicle day. LimePass adoption also became a larger contributor, representing 28% of 2025 revenue compared with 20% in 2024, suggesting deeper rider engagement and more recurring usage behavior.

Operating performance improved significantly as Lime scaled its platform. The company generated an operating loss of $24.6 million in 2023 before producing operating income of $47.0 million in 2024 and $70.4 million in 2025. The progression highlights the operating leverage embedded within the business as rider density, fleet utilization and city-level economics continue to improve.

Gross profit increased from $169.2 million in 2023 to $281.1 million in 2024 and $345.4 million in 2025. Gross margin improved sharply from 32.4% in 2023 to 40.9% in 2024 before moderating to 39.0% in 2025 as cost of revenue grew faster than revenue. The 2025 margin compression appears tied to targeted operating investments, fleet reliability initiatives and higher depreciation and amortization associated with the company's vehicle base. Even with that moderation, Lime is operating at a substantially healthier gross margin profile than the micromobility sector historically produced.

Adjusted Gross Profit, which excludes depreciation and amortization and certain vehicle disposal costs, increased from $276.3 million in 2023 to $368.6 million in 2024 and $467.2 million in 2025. Adjusted Gross Margin remained relatively stable at 52.9% in 2023, 53.7% in 2024 and 52.7% in 2025. This is an important metric for investors because it highlights the underlying ride-level and city-level economics before the impact of asset depreciation. The stability of adjusted gross margins suggests Lime has reached a more mature unit economic model, even as it continues to expand fleet size and geographic reach.

Adjusted EBITDA also improved meaningfully. Lime generated Adjusted EBITDA of $99.8 million in 2023, $153.4 million in 2024 and $218.1 million in 2025. Adjusted EBITDA margin expanded from 19.1% in 2023 to 22.3% in 2024 and 24.6% in 2025. This reflects a business that is no longer simply scaling revenue, but also demonstrating meaningful corporate operating leverage. The company's fixed-cost structure, larger fleet base and increasing rider density appear to be translating into improved profitability as revenue grows.

GAAP profitability remains less clean. Lime reported net losses of $122.4 million in 2023, $33.9 million in 2024 and $59.3 million in 2025. The wider net loss in 2025, despite stronger revenue and Adjusted EBITDA, reflects below-the-line and non-cash items, including interest expense, fair value adjustments and other expenses. Investors will likely focus on the gap between strong Adjusted EBITDA and continued GAAP losses, particularly as the company transitions into the public markets and works to simplify its capital structure.

Cash flow trends are one of the stronger parts of the story. Net cash provided by operating activities increased from $81.2 million in 2023 to $169.0 million in 2024 and $214.8 million in 2025. Free Cash Flow increased from $1.1 million in 2023 to $47.3 million in 2024 and $103.8 million in 2025. This is notable because micromobility is a capital-intensive model that requires ongoing vehicle purchases, repair investment and fleet deployment. Lime's ability to generate positive Free Cash Flow while growing revenue nearly 30% in 2025 should be a central point of institutional interest.

First-quarter 2026 results continued to show growth, though seasonal weakness remains visible. Revenue increased 32% year-over-year, while gross profit increased to $44.6 million from $28.9 million in the prior-year period. Adjusted Gross Profit increased to $74.2 million from $56.5 million, and Adjusted EBITDA improved to $7.5 million from $2.1 million. However, Lime still reported a net loss of $61.3 million in the quarter, compared with a net loss of $56.0 million in the prior-year period. Free Cash Flow was negative $79.2 million in the first quarter, reflecting the seasonal nature of the business and the timing of vehicle capital expenditures ahead of the stronger spring and summer riding seasons.

The balance sheet will also be an important focus. As of March 31, 2026, Lime reported $261.3 million of cash and cash equivalents. On an as-further-adjusted basis, reflecting the IPO and repayment of debt, cash would increase to approximately $290.7 million. Stockholders' equity would improve from a deficit of ($565.7 million) to approximately $577.0 million, while approximately $114.2 million of outstanding term loan borrowings would be repaid. The offering should significantly simplify Lime's capital structure through the conversion of preferred stock and convertible securities into common equity.

From a market perspective, Lime is coming public as a scaled category leader in a sector that has already gone through a major shakeout. Many earlier shared mobility companies struggled with weak vehicle durability, poor unit economics, regulatory friction and limited path to profitability. Lime's current financial profile is meaningfully different: revenue is approaching $900 million, Adjusted EBITDA is above $200 million, Free Cash Flow is positive on a full-year basis and the company has demonstrated improved operating discipline.

Investors evaluating the offering will likely focus on the durability of revenue growth, the sustainability of Adjusted EBITDA margins, the capital intensity of fleet expansion, city-level regulatory risk, seasonality, dependence on Uber as a distribution partner and the company's ability to narrow GAAP losses. The key debate will be whether Lime should be valued as a profitable transportation technology platform with strong local network effects, or as a capital-intensive urban mobility operator exposed to regulation, weather, depreciation and fleet replacement cycles.

With global scale, strong brand recognition, improving margins and a materially better cash flow profile than earlier micromobility models, Lime is positioned to be one of the more closely watched consumer transportation technology IPOs of 2026.