Space Exploration Technologies Corp. (SPCX) officially filed its S-1 registration statement today...

When most companies go public, investors spend their time evaluating the business. They study the financials, compare valuations, and decide whether the opportunity justifies the risk. SpaceX is different. By the time the company reaches the public market, much of that debate has already taken place.

Instead, the real story surrounding SpaceX's June 12 debut is what it says about the market itself.

For nearly four years, the IPO market has worked its way back from one of the most challenging periods in recent memory. Rising interest rates, inflation concerns, and risk aversion forced many private companies to delay public offerings. Deal sizes shrank, valuations compressed, and investors became increasingly selective. While the market gradually recovered, many wondered whether public investors would once again support the kind of transformative companies that historically defined great IPO cycles.

SpaceX may provide that answer.

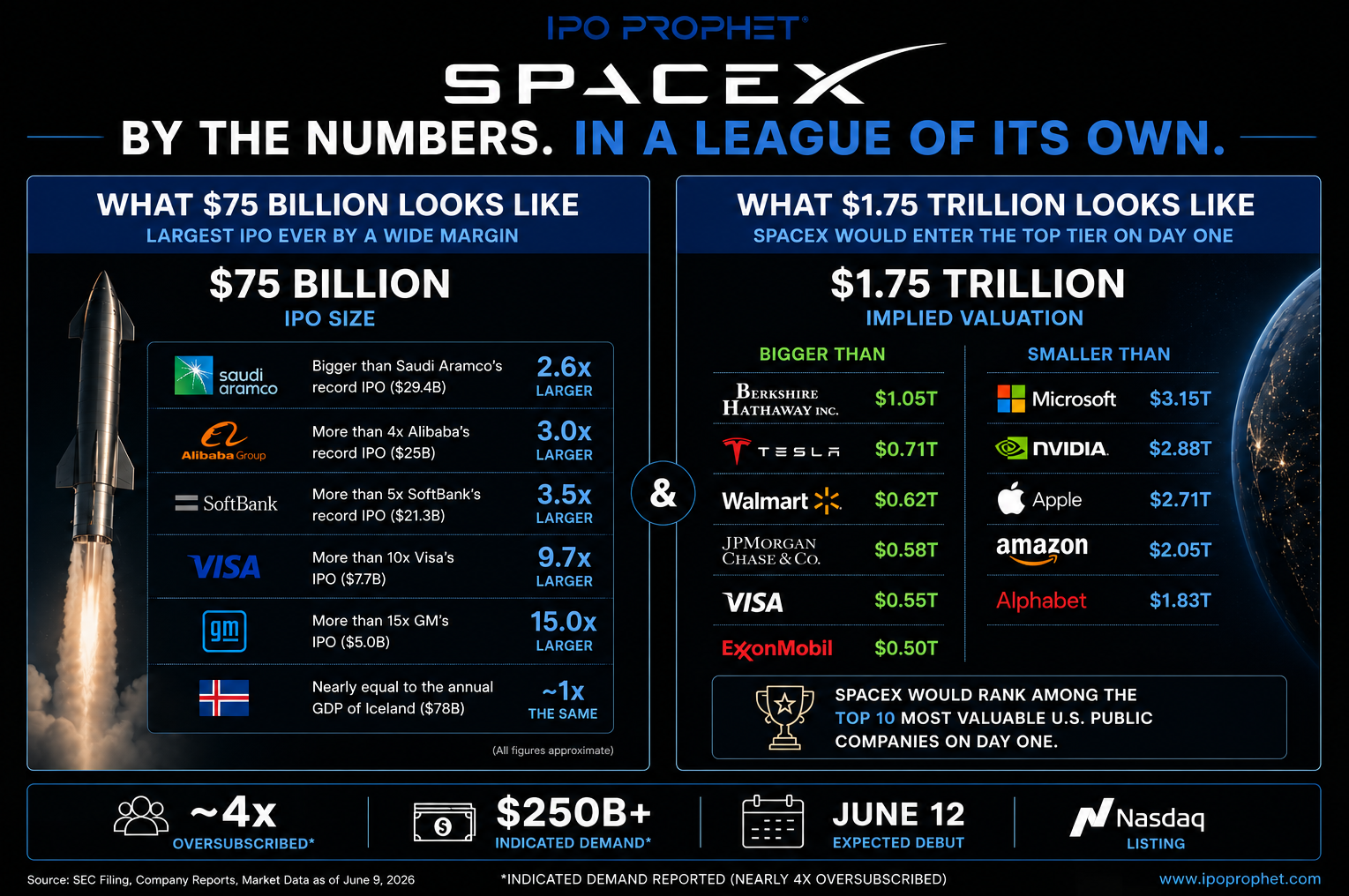

This is not simply another large offering. At approximately $75 billion in proceeds and a valuation approaching $1.75 trillion, SpaceX represents a scale rarely seen in public markets. More importantly, it represents a company that could have remained private indefinitely. Unlike traditional IPO candidates, SpaceX is not coming public because it needs capital to survive or expand. It is coming public after spending more than two decades proving its business model, building dominant market positions, and attracting virtually unlimited private investment.

That distinction matters.

For years, investors have argued that the most valuable companies now stay private longer than ever before. In many cases, public investors were left watching from the sidelines as significant value creation occurred in private markets. SpaceX may signal a shift in that dynamic. Rather than serving as an example of why companies remain private, it may demonstrate why the public market still matters.

The public market remains the deepest pool of capital in the world. It provides liquidity, transparency, broad ownership, and the ability for millions of investors to participate in the growth of industry-leading companies. A successful SpaceX debut would reinforce that the public market remains the ultimate destination for even the most sought-after private enterprises.

The implications extend well beyond a single company. Every private market leader is watching this transaction closely. If investors enthusiastically absorb an offering of this magnitude, it could create a roadmap for the next generation of mega-cap private companies. Firms such as Stripe, Databricks, Anthropic, OpenAI, and others may view the reception to SpaceX as evidence that public investors are once again willing to support category-defining businesses at scale.

That is why this offering matters far beyond aerospace, satellite communications, or space exploration.

The success of SpaceX will not be measured solely by where the stock opens on June 12 or where it closes that afternoon. Its broader significance lies in what it says about investor confidence, capital formation, and the continued evolution of the IPO market itself.

For years, market participants have asked whether the IPO market could return to supporting the largest and most ambitious companies in the world. SpaceX may provide the answer.

The question is no longer whether SpaceX is ready for the public market.

The question is whether the public market has proven it is ready for SpaceX.