MiniMed Group, Inc., the diabetes business being separated from Medtronic, has filed to go public in an offering that could raise approximately $728 million. The company plans to offer 28,000,000 shares at a proposed price range of $25.00 to $28.00 per share and intends to list on the Nasdaq Global Select Market under the ticker “MMED.” At the midpoint price of $26.50 and based on approximately 280.8 million shares expected to be outstanding following the offering, MiniMed would carry an implied market capitalization of roughly $7.4 billion. Goldman Sachs, BofA Securities, Citigroup, and Morgan Stanley are leading the deal. Medtronic is expected to retain majority voting control following the offering, positioning MiniMed as a “controlled company” under Nasdaq rules.

Net proceeds to the company are estimated at approximately $712 million at the midpoint, after underwriting discounts and expenses. As part of the separation from Medtronic, MiniMed intends to retain roughly $350 million of proceeds for general corporate purposes, with the remaining proceeds expected to be used to repay intercompany debt owed to Medtronic or related affiliates and to settle certain separation-related obligations. The allocation suggests the IPO is both a capital-raising event and a balance sheet restructuring tied to the carve-out, positioning MiniMed with greater financial flexibility as a standalone entity.

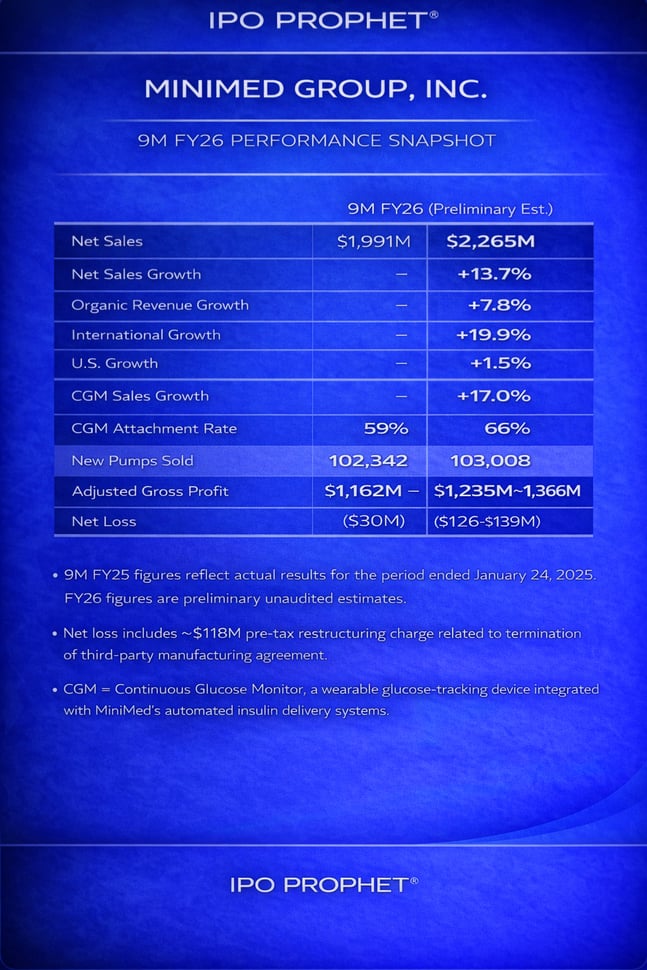

Unlike early-stage medtech IPOs, MiniMed enters the public markets as a scaled commercial operator. For the nine months ended January 23, 2026, the company generated $2.27 billion in net sales, representing 13.7% reported growth over the comparable prior-year period. On an organic basis — excluding currency impacts and adjustments tied to Italian payback accruals — revenue increased 7.8%, reflecting steady underlying expansion across its insulin pump and continuous glucose monitoring ecosystem. International markets remain the primary growth engine, with revenue outside the United States increasing 19.9% year-to-date compared with 1.5% growth domestically. The divergence highlights stronger overseas adoption trends, particularly following the launch of the Simplera CGM platform in Europe, as well as competitive and product timing pressures in the U.S. earlier in the fiscal year.

Continuous Glucose Monitor (CGM) adoption remains a central structural driver of the business. CGM sales increased 17.0% for the nine-month period, while the global CGM attachment rate rose to 66%, up from 59% in the comparable prior-year period. Higher attachment rates drive recurring revenue per patient, deepen integration within MiniMed’s automated insulin delivery platform, and support longer-term revenue durability. The shift toward CGM-integrated systems strengthens the company’s consumables mix and enhances ecosystem stickiness, particularly in international markets where growth has accelerated more rapidly.

Profitability metrics reflect both operational scale and transitional noise. Adjusted gross profit for the nine months ended January 23, 2026 is estimated between $1.24 billion and $1.37 billion, compared with $1.16 billion in the prior-year period, demonstrating healthy gross margin generation on an adjusted basis. Reported net loss is expected to widen to a range of $(126 million) to $(139 million), versus $(30 million) in the comparable period. The increase is largely attributable to an approximately $118 million pre-tax restructuring charge tied to the termination of a third-party manufacturing agreement approved in December 2025. Excluding this one-time charge, underlying operating performance appears considerably more stable than headline GAAP figures suggest.

The bull case for MiniMed centers on its scale, recurring revenue profile, and expanding international footprint. With more than $2 billion in annualized revenue and improving CGM penetration, the company operates at meaningful commercial scale in a large and growing global diabetes market. If U.S. growth stabilizes, manufacturing transition risk subsides, and CGM attachment continues to increase, margin expansion and operating leverage could follow. At an implied $7–8 billion valuation, MiniMed may appeal to investors seeking exposure to a durable medtech platform with established revenue rather than clinical-stage uncertainty.

The bear case focuses on competitive dynamics, carve-out execution risk, and governance structure. The U.S. diabetes device market remains highly competitive, with strong incumbent players in CGM and pump technologies. Domestic growth has been modest relative to international markets, and sustained competitive pressure could weigh on margins. As a controlled company, MiniMed will remain majority-owned by Medtronic, limiting governance influence for public shareholders. Additionally, the separation process, supply chain transition, and reimbursement variability introduce operational and regulatory risks that could affect near-term performance.

Overall, MiniMed’s IPO represents a large-scale medtech carve-out entering the public markets with substantial revenue, expanding recurring product mix, and transitional restructuring impacts. The offering combines growth, scale, and separation dynamics, positioning MiniMed as a mature diabetes technology franchise seeking standalone market visibility and capital flexibility. At a multibillion-dollar implied valuation, the deal stands out as one of the more significant medtech listings in the current IPO cycle, offering investors exposure to a revenue-generating diabetes platform balancing steady expansion with competitive and execution risk.

MiniMed Group is expected to make its Nasdaq debut on March 6th, 2026.