Kailera Therapeutics is moving toward the public markets with plans to offer 33.3 million shares at a range of $14 to $16, implying a midpoint deal size of approximately $500 million and a post-offer market cap of roughly $1.8 billion, as the clinical-stage biotechnology company looks to position itself in the rapidly expanding obesity therapeutics market. The company has applied to list on the Nasdaq Global Select Market under the ticker “KLRA”, with J.P. Morgan, Jefferies, Leerink Partners, TD Cowen, and Evercore ISI serving as joint bookrunners.

At its core, Kailera is an advanced clinical-stage biotech focused exclusively on obesity, building a diversified pipeline centered around GLP-1–based therapies, the same class that has driven the explosive growth of drugs like semaglutide and tirzepatide. Rather than being an early entrant, the company is positioning itself as a next-generation player, aiming to push efficacy, tolerability, and treatment flexibility beyond what current therapies offer—particularly for higher-BMI patients where unmet need remains significant.

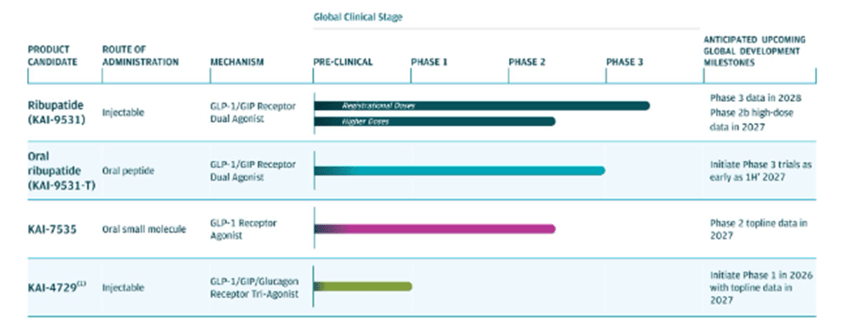

The story is anchored by its lead asset, ribupatide (KAI-9531), a once-weekly injectable GLP-1/GIP dual agonist currently in global Phase 3 trials. Kailera believes ribupatide has the potential to deliver category-leading weight loss, supported by early clinical data showing up to ~23% mean weight reduction at higher doses over 12 weeks and ~17–19% reductions in longer-duration trials, with no observed plateau in efficacy. While these results are compelling, the company has not conducted head-to-head trials against leading therapies, leaving relative positioning versus incumbents an open question.

Beyond its lead program, Kailera is building what it views as a full-spectrum obesity franchise, targeting patients across the treatment continuum. This includes an oral version of ribupatide designed to improve convenience and tolerability, a small molecule GLP-1 agonist (KAI-7535) aimed at broader scalability, and a next-generation triple agonist (KAI-4729) incorporating glucagon activity to potentially enhance weight loss and metabolic outcomes. The pipeline reflects a strategy not just to compete within the GLP-1 category, but to expand it across modalities and mechanisms.

A key structural advantage is Kailera’s strategic collaboration with Jiangsu Hengrui Pharmaceuticals, which provides access to extensive clinical data generated in China and allows the company to accelerate global development while maintaining capital efficiency. Kailera holds exclusive commercialization rights outside Greater China, leveraging Hengrui’s development engine while focusing its own efforts on global regulatory and commercial execution.

From a market perspective, the opportunity is significant. Obesity affects over 1 billion people globally, with the fastest-growing segment consisting of patients with BMI ≥35, a population that continues to show incomplete response even with current leading therapies. Kailera is explicitly targeting this gap, emphasizing greater magnitude of weight loss as its primary differentiator rather than incremental improvements.

Kailera’s financial profile reflects its early-stage, investment-heavy operating model, with no revenue generated to date. For the year ended December 31, 2025, the company reported a net loss of approximately $149.0 million, compared to a $219.7 million loss in its initial operating period in 2024, which included a significant $214.1 million in-process R&D charge tied to its licensing agreement with Hengrui. Excluding this one-time item, operating expenses ramped meaningfully in 2025, with research and development increasing to $109.1 million and general and administrative expenses rising to $49.2 million, reflecting the advancement of its clinical pipeline. On the balance sheet, Kailera reported approximately $160 million in cash and equivalents as of year-end 2025, which is expected to increase to roughly $600+ million on a pro forma basis following the IPO, providing a multi-year runway to fund its Phase 3 programs and broader pipeline development.

That said, the risk profile remains consistent with the biotech sector. Kailera is pre-commercial, with all product candidates still in clinical development, and key value inflection points tied to Phase 3 readouts expected in 2027–2028. The company is also entering one of the most competitive therapeutic areas in the market, where incumbents continue to invest heavily in next-generation obesity treatments. Clinical, regulatory, and competitive risks remain central to the investment case.

Overall, Kailera enters the IPO market as a high-beta obesity play, combining a differentiated pipeline strategy with early data that suggests meaningful upside—but with execution risk that will ultimately be defined by late-stage clinical outcomes. In a market increasingly focused on the next wave of GLP-1 innovation, Kailera is positioning itself as a second-generation contender aiming to raise the bar on efficacy while expanding access across treatment modalities.

Kailera is expected to price later this week and begin trading on Friday, April 17.